Most beginners pick a number that feels right: 10 shares, 50 shares, 100 if the stock is cheap. The right answer to how many shares you should buy depends on three inputs: your account size, how much you're willing to lose on the trade, and where your stop loss sits. Get those three inputs right and you have your share count.

Key Takeaways

- The share count is a formula output from three values: account size, risk percentage and stop distance.

- Most traders cap risk at 1–2% of account equity per trade; higher numbers compound losses into drawdowns that are hard to recover from.

- The core formula is shares = (account size × risk%) ÷ (entry price − stop loss price).

- Fractional shares at most major US brokers let you apply the formula without rounding, even on small accounts.

- Position sizing controls long-term survival more than stock selection does; a trader who sizes to the formula can survive a string of bad picks.

The Simple Approach (And Why It Falls Short)

Most beginners run this calculation: take the dollars you want to spend, divide by the stock price, buy that many shares. You have $2,000 and the stock trades at $50, so you buy 40 shares. That math works fine for a long-term investor who plans to hold for years and can absorb short-term volatility. It answers "how much of this company do I want to own?"

For an active trader, it answers the wrong question. Knowing how many dollars went in tells you nothing about how many dollars are at risk. A trader who puts $2,000 into a stock without a defined exit point has no idea whether a bad trade costs $50 or $600. If you're paper trading before going live, start with risk-based sizing. Dollar-based sizing hides the actual risk.

The Right Question to Ask

Ask "how much am I willing to lose if this trade fails?" instead. That dollar amount is your risk per trade, and it controls position size.

Say you're willing to lose $100 on a trade. Your stop loss is $2.50 below your entry. You can buy 40 shares ($100 ÷ $2.50). If the stock hits your stop, you lose exactly $100. You set risk first and calculate shares second.

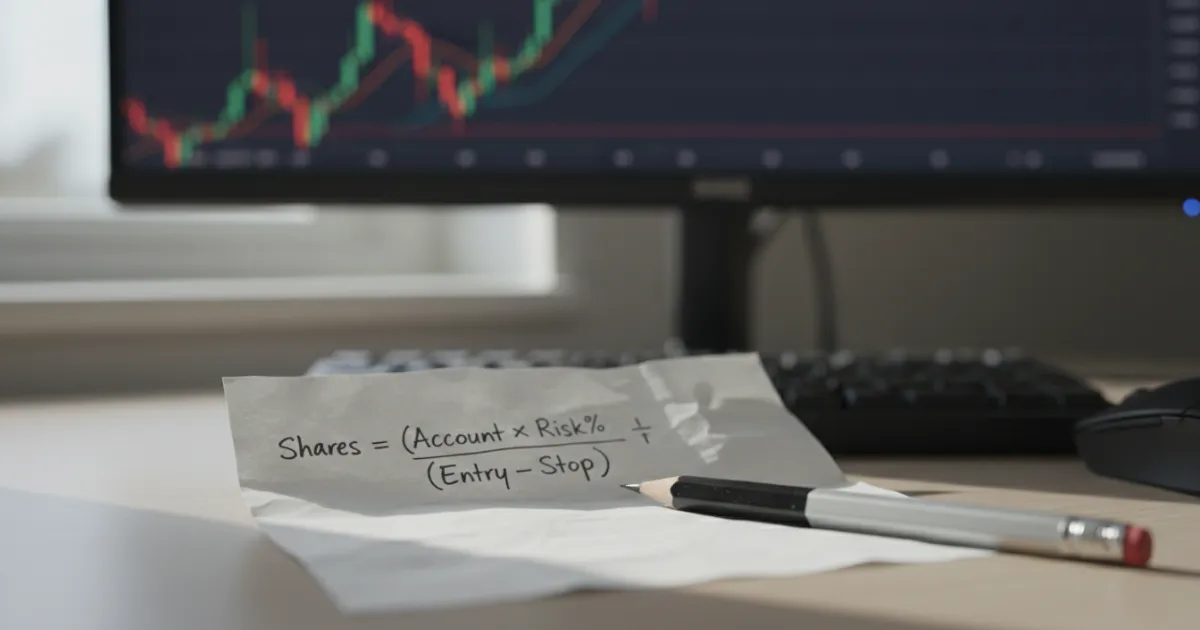

The Risk-Based Formula

Shares = (Account Size × Risk%) ÷ (Entry Price − Stop Loss Price)

You need three inputs.

Account size. Use your current account equity. A target figure distorts the math.

Risk percentage. The fraction of your account you're willing to lose on this single trade. Van Tharp's work on fixed-fractional position sizing puts the sustainable range at 1–2% per trade. Risk 1% on a $10,000 account and your maximum loss per trade is $100. Risk 5% and four consecutive losses cut 20% off your account. The math compounds fast in both directions.

Risk per share. Entry price minus stop loss price. That number is what you lose on each share if the trade goes wrong. A stock entered at $50.00 with a stop at $47.50 has a risk per share of $2.50. Tighten the stop to $49.00 and risk per share drops to $1.00. At the same dollar risk, you can buy more shares. Your stop placement sets how many shares fit in the formula. For how stop placement interacts with profit targets, see What Is Risk to Reward Ratio?

For an advanced framework that sizes based on your edge's win rate and payoff ratio, the Kelly Criterion is the next step up. For most beginners, fixed-fractional sizing is the right starting point.

A Worked Example

Account size: $10,000. Risk per trade: 1% ($100). Stock entry: $50.00. Stop loss: $47.50. Risk per share: $2.50.

Shares = $100 ÷ $2.50 = 40 shares

Total position value: $2,000 (20% of account). Maximum loss on the trade: $100 (1% of account).

Now consider what happens without the formula. Same trader, same stock, but they decide to buy 200 shares because the chart looks strong. Position value: $10,000, their entire account in one trade. If the stock drops to $47.50, they lose $500, or 5% of the account on a single loss. Three losses like that and you're down 15% before the month ends.

The Position Size Calculator runs this math for you if you'd rather not do it by hand each time.

What Happens When You Size Too Large

Lose 10% of your account and you need an 11% gain to get back to flat. Lose 25% and you need 33%. Lose 50% and you need 100% to recover. Each percentage point of drawdown raises the recovery bar higher than the loss that caused it.

Oversizing also distorts behavior trade by trade. Research by Barber and Odean documented that retail investors who trade with high frequency underperform. A trader with too much on the line makes worse decisions: they cut winners early to lock in a cushion and hold losers longer to avoid confirming the loss.

You see the same pattern with overtrading. A trader in an oversized position feels pressure from every price tick and manufactures reasons to act. The Risk of Ruin Calculator models what happens to ruin probability when per-trade risk climbs too high across a realistic losing streak.

Account Size, Fractional Shares, and the PDT Change

Fractional shares

Small accounts don't have to round up to the nearest full share anymore. Schwab, Fidelity, and most major US brokers now support fractional share trading, so a $1,000 account can apply the risk-based formula to the decimal. If the formula outputs 7.3 shares, you buy 7.3 shares.

The Pattern Day Trader (PDT) rule change

The Pattern Day Trader (PDT) rule is gone. On April 14, 2026, the SEC granted accelerated approval to FINRA's proposed rule change SR-FINRA-2025-017 (SEC Release No. 34-105226), removing the $25,000 minimum equity requirement and the PDT designation from FINRA Rule 4210. FINRA is replacing the day-trading margin framework with intraday margin standards based on real-time position risk rather than a fixed day-trade count.

Timing: FINRA will publish a Regulatory Notice announcing an effective date 45 days after that notice appears, and member firms have up to 18 months from the same publication date to complete their system changes. Day-to-day mechanics at any given broker depend on where that broker is in its rollout. If you're an active trader on a small account, check with your broker for their current status before assuming any specific behavior.

T+1 settlement

Cash accounts carry a separate constraint that hasn't changed. US equities settle on a T+1 cycle following the SEC's 2023 rule change, effective May 2024. Capital tied up in an unsettled trade can't be redeployed the same day. For active traders on small cash accounts, this limits how many concurrent positions are practical. That alone argues for keeping per-trade size small.

Common Sizing Mistakes

Sizing by conviction. "I really like this setup" isn't a formula input. Traders who size up on conviction mismanage those trades more often than any other category.

Using the same share count on every trade. 100 shares of a $5 stock is a $500 position. 100 shares of a $200 stock is a $20,000 position. Same share count, different risk exposure. The formula accounts for price; a fixed share count doesn't.

Ignoring the stop loss distance. Two trades can have identical dollar position sizes but different risk profiles depending on where the stop sits. A $2,000 position with a stop 1% away risks $20. The same $2,000 position with a stop 10% away risks $200. Position size without stop placement is half a calculation.

Scaling up after a winning streak. A few good trades don't change the probability of the next one. The trader who ratchets risk up after wins and pulls it back after losses is running a different system than the one they wrote down in their trading journal.